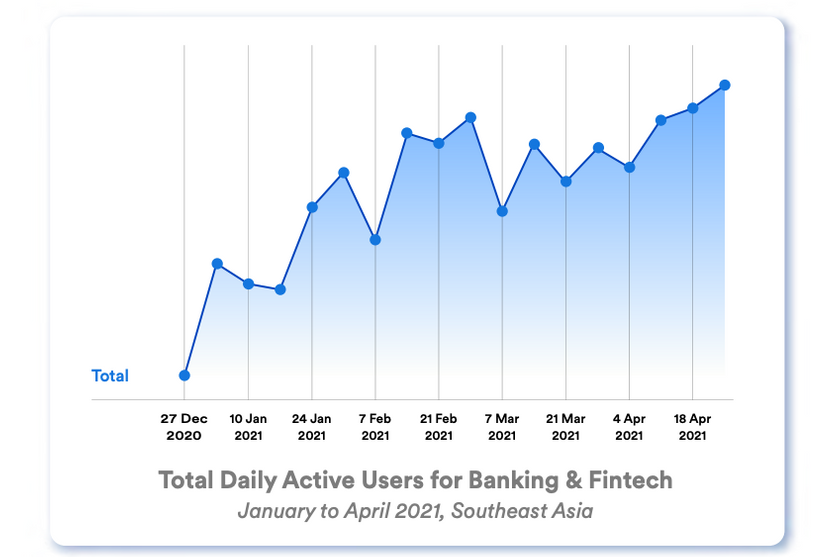

The Singapore Business Times reports that in the Asia-Pacific region, more than 21% of the population is unbanked. This is most apparent in Southeast Asia, where more than 44% of people do not have bank accounts. The disparity between the banked and unbanked in the region creates opportunities for digital financial services to close the gap, with the acceleration in adoption already being seen in Southeast Asia. A 2021 report from MoEngage reports a 55% increase in daily users across all digital banking activities.

This movement is led primarily by millennials and Gen Z, who have readily embraced services from online banking to digital wallets. In Singapore and Vietnam, for example, commercial banks have launched digital banking solutions targeted specifically for their younger consumers. UOB, a Singaporean multinational investment bank and financial services company, launched TMRW, an AI-powered mobile-only bank. And MSB, Vietnam’s leading commercial bank, launched TNEX, the first digital-only bank in the country.

Another fast-emerging trend is mobile payments, stemming from the increased usage of mobile phones in Southeast Asian markets. The Fintech Times reports that in the Philippines, there are at least 1.59 mobile phones for every person. Acceptance of mobile payments by both consumer and retailer has paved the way for non-financial companies like Grab, a leading mobile app for transportation and food delivery services in Southeast Asia, and regional e-commerce platforms like Lazada and Shopee, to offer their consumers new cash payment methods.

While giants like Apple, Google, Alibaba, and Tencent have led the way for card-based mobile wallets in more developed markets, stored value mobile wallets are more popular in emerging markets. Credit-card and debit-card usage are lower in the latter, paving the way for local players to grab a share of the growing pie. Some of the top mobile wallet players are GCash (Philippines), GrabPay (Malaysia), Ovo (Indonesia), TrueMoney (Thailand), and MoMo (Vietnam), per a 2021 Boku report.

The growth of digital finance technology and adoption is uncovering new opportunities for marketers in 2022 and beyond, and there are four ways in which these opportunities could be unlocked.

1. Delivery of hyper-targeted ads and end-to-end experiences

The growing scale and data captured by apps with digital finance components provide opportunities for hyper-targeted advertising, where audiences are selected based on their financial capability and purchasing behaviour. Moreover, the loop from awareness to purchase to loyalty can be closed all in a single platform.

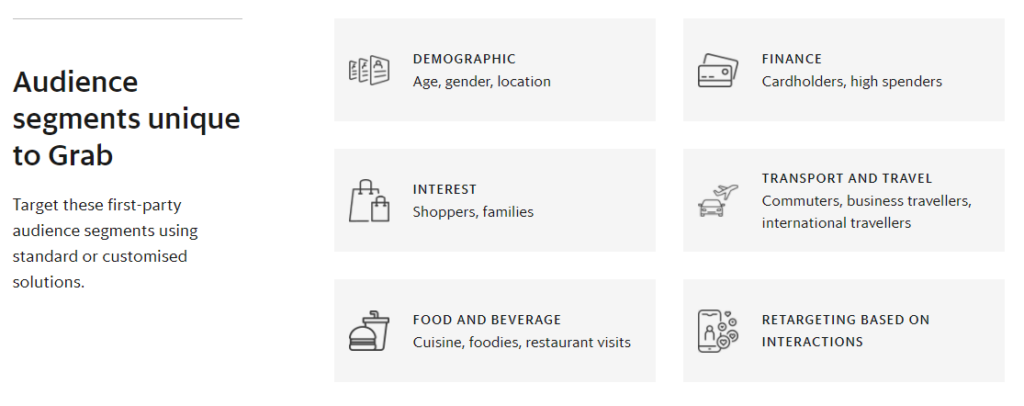

Grab is one of the largest mobile apps in Southeast Asia with a 142m estimated number of users from 400 cities and towns. GrabPay, its financial arm, has been showing robust growth with total payments increasing by 60% year-on-year. The app allows for targeting of audiences based on day-to-day transactions and activities such as the type of card and size of spending along with restaurant visits and shopping behaviours, going beyond the typical interest and affinity-based targeting that relies on proxies of engagement.

Alongside targeting the right audiences, marketers can drive awareness and consideration through Grab’s placement assets, conversions are fluidly done through GrabFood or GrabMart and loyalty points can be provided through GrabRewards.

2. Providing more meaningful offers and incentives

Based on the survey of global insurance provider Swiss Re, 58% of respondents across Southeast Asian markets actively searched for new insurance policies during the pandemic and nearly half are open to purchasing new policies because of the outbreak. Digital finance companies are increasing the accessibility of policies through micro-insurance with low cash outlays, especially appealing to Gen Z and millennials.

Marketers can now use digitally distributed policies to make offerings and incentives more relevant for younger generations. For instance, Digi Telecommunications, a mobile service provider in Malaysia, partnered with AXA Affin, a multinational insurance and finance company, to provide free life insurance to its new prepaid plan subscribers. Similarly, Tiki, an e-commerce site in Vietnam, partnered with FWD, a life insurance company, to provide free coverage for 100,000 customers.

3. Scaling promotions beyond point-of-purchase

One of the key benefits of digital finance is the ease of distribution of digital vouchers and rewards. Mobile wallets are already being used as distribution channels for relief funds or e-vouchers of food and medicine. Brands can capitalize on this phenomenon through digital-based promotions and sampling, giving them a broader scale versus on-ground activations. This is especially relevant in the pandemic environment wherein mounting events or delivering items are more challenging due to varying restrictions. Instead of manually handing out coupons and prizes, marketers can now partner with e-wallet apps for cashback promos and automated rewards redemption.

4. Increasing the accessibility of products and services

Traditionally, purchasing big-ticket items can only be done by the small base of affluent consumers paying with cash or with credit cards. Today, even the unbanked can pay in instalments with convenient applications and fast approvals through e-commerce platforms. Ecommerce platform Lazada partners with financial apps in the Philippines and offers LazPayLater in Indonesia to allow non-credit card customers to pay in increments. Shopee offers SPayLater in Indonesia and Thailand, wherein loans of select unbanked customers are approved in as fast as 10 minutes.

As more consumers try to stretch their money, they will be more open to purchasing in instalments with minimal interest. Instead of relying solely on credit cards, marketers now have the option to expand their financial partners to e-commerce websites and digital loan providers to enable more audiences to buy their products.

Digital finance adoption is accelerating as consumers become more knowledgeable about the industry’s products and services. Digital finance has created new possibilities for brands and retailers across a myriad of marketing touchpoints, and marketers should be capitalizing on these opportunities to be the first in reaping its benefits.

This article was written by Elizabeth Shie, senior regional strategist at UM APAC, and Abygayle Brani, regional marketing & communications strategist at UM APAC.

The article is published as part of MARKETECH APAC’s thought leadership series What’s NEXT. This features marketing leaders sharing their marketing insights and predictions for the upcoming year. The series aims to equip marketers with actionable insights to future-ready their marketing strategies.

If you are a marketing leader and have insights that you’d like to share with regards to the upcoming trends and practices in marketing, please reach out to [email protected] for an opportunity to have your thought-leadership published on the platform.

![[Campaign] Sunsilk x BABYMONSTER](https://marketech-apac.com/wp-content/uploads/2026/07/Campaign-Sunsilk-x-BABYMONSTER.webp)