Financial services company HSBC has unveiled that it will host an exclusive ‘League of One’ party with South Korean League of Legends (LoL) team T1 and esports legend Faker to promote esports in Hong Kong.

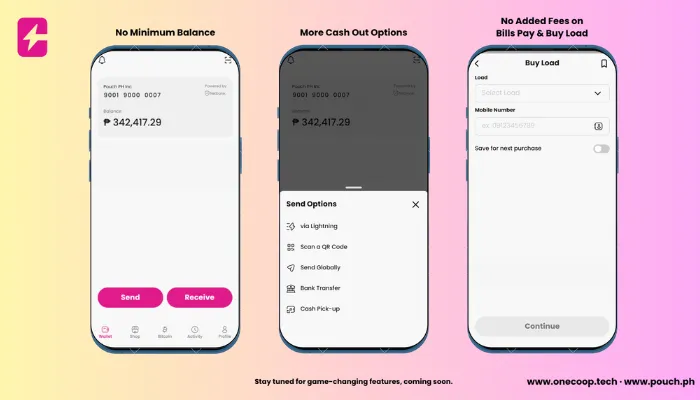

Manila, Philippines – Aiming to provide Filipinos with better financial services, Pouch.ph has recently announced a collaboration with One Cooperative Technology Service (OCTS), introducing its first and only CDA-registered technology service cooperative mobile wallet. Known as CoopPay, the platform...

Almost 60% of consumers in the Asia-Pacific have expressed interest in AI-driven decision-making facilitation for their investments amid economic uncertainty and perceived financial crises, a report from dentsu revealed.

Around 79% say they use mobile apps to look after their personal finances—the second highest figure in Asia after that of India. The age-group differences are narrower compared with those for mobile health, and more 45-55 year olds use finance apps (68%) than use health apps (58%).

FSTI 3.0 will continue to support advanced capability development and adoption in key areas such as artificial intelligence and data analytics (AIDA), and Regulation Technology (RegTech).

The successful large fundraiser comes amidst a global slowdown in fintech growth and funding. Despite the difficult financial market conditions, Endowus has continued to experience accelerated growth with group assets now crossing US$5b.

By integrating Ptarmigan's specialized media and marketing solutions designed for financial services brands, Omnicom will benefit from its expertise in the industry.

Liu will be responsible for overseeing American Express' issuing businesses across the Hong Kong, Taiwan, Singapore and Thailand markets.

The equity funding by TNG Digital was made through an investment by the Lazada Group, as well as from its parent company Touch ‘n Go Group.

The partnership will help women in rural communities of Bangladesh access affordable small business loans.